When making decisions about your Medicare coverage, you may be faced with the choice of either having a Medicare Supplement or a Medicare Advantage Plan. This is especially true when you are new to Medicare. Medicare Supplements and Medicare Advantage plans are the two ways to set yourself up with extra coverage & fill the gaps in Medicare. These are two very different types of plans and your choice is one or the other; you cannot have both. With that said, it’s important to understand the differences between the two and the future implications of any decisions that you make.

Medicare Supplement Vs. Medicare Advantage Overview

Medicare Supplements are insurance plans that are secondary to Medicare A & B. To have a Medicare Supplement, you must be enrolled in “Original Medicare.” This means you have Medicare Part A & B directly through the Centers for Medicare & Medicaid, a department of the federal government. With Medicare A & B being your primary insurance, Medicare Supplements are designed to give you more coverage and lower out of pocket medical costs. Hence, more protection and peace of mind. When you have a Medicare Supplement, you will also need separate prescription coverage (Part D), and any other extra benefits that you want. Having this setup is like being at an “a la carte” buffet, piecing together the benefits that you want & need.

Medicare Advantage is when you receive your Medicare coverage through a private insurer and is also known as “Part C.” Medicare Advantage Plans include all of your benefits in one package. This includes Part A, B, D (drug), and potentially other extra benefits like dental & vision. If Medicare Supplements are like being at a buffet, Medicare Advantage Plans are like a “Value Meal.” Within this package you also have networks, which are the doctors and hospitals that have agreed to accept the plan. The two most popular type of Medicare Advantage Plans are HMO’s & PPO”s, each of which have their rules on how you can access doctors.

Being covered by either of these types of plans is better than just having Medicare A & B by itself. Having only Medicare A & B can be equated to getting the radio without the batteries or the car without lug nuts fixed to the wheels. There are many reasons to have either a Medicare Supplement or Medicare Advantage vs. just Medicare. The main reason being out of pocket maximums. If you have only Medicare A & B, you’ll have deductibles and co-insurance without any annual limits. Both Medicare Supplements and Medicare Advantage help you by limiting your out of pocket medical costs and making them more predictable.

Comparing Medicare Supplements Vs. Medicare Advantage In 5 Areas

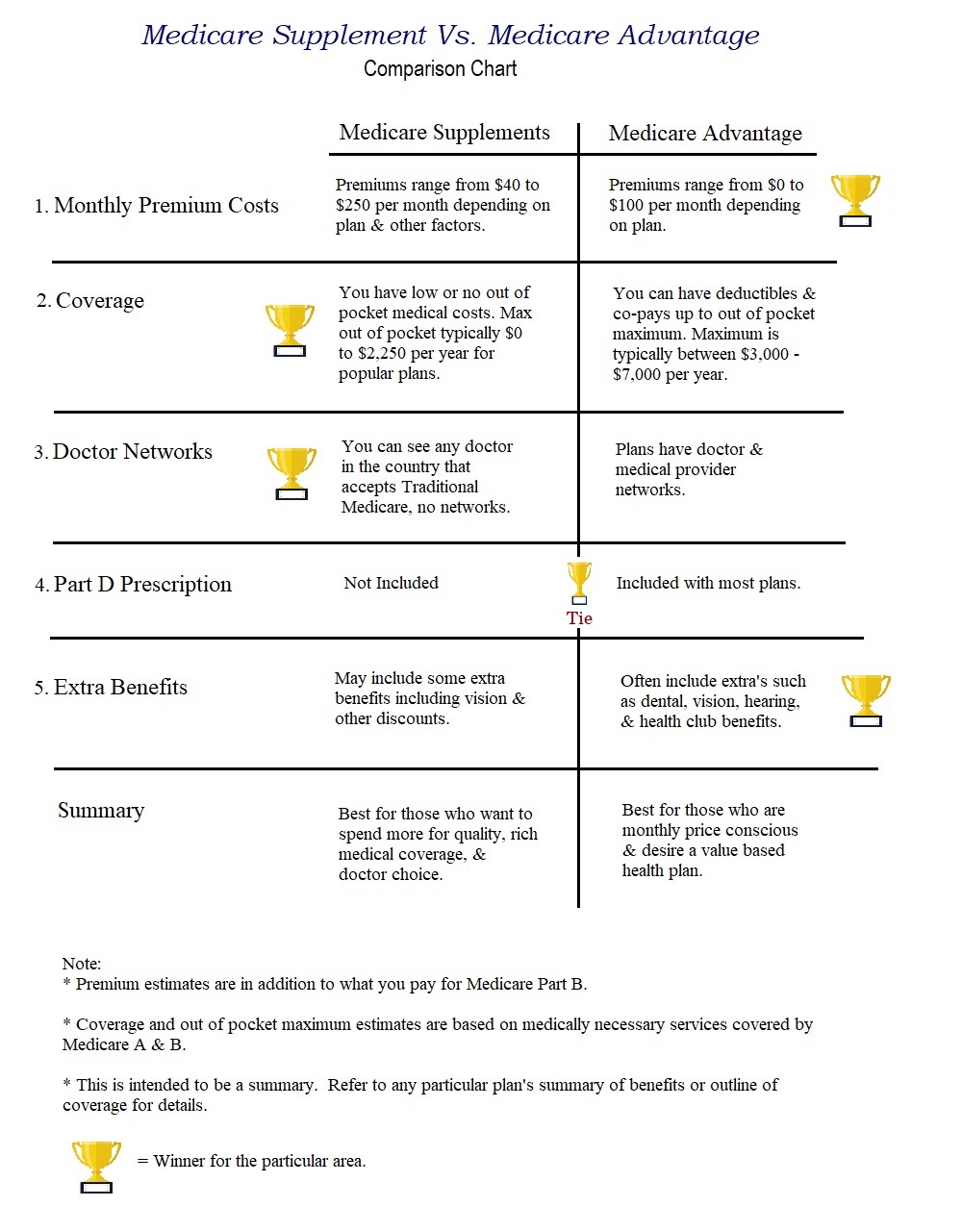

In my experience, the differences between Medicare Supplements & Medicare Advantage break down into 5 key areas. In the sections below I will break down these 5 areas and assign a winner between the two plan types. Let’s start with a comparison chart chart to get a visual overview and then we’ll dig into the details.

Area 1 – Monthly Premium Costs

The first area of consideration is monthly premium costs. The good news is, relative to other types of medical insurance, many find both Medicare Supplements & Medicare Advantage plans to be affordable. The first thing to keep in mind is that the monthly premium you pay for either of these type of plans is in addition to what you pay for Medicare. You can see the most up to date Medicare premium costs by clicking here and visiting Medicare’s site.

Medicare Advantage Plans have lower premium costs vs. Medicare Supplements. On the low end, Medicare Advantage Plans start at $0 monthly premium. In fact, there are even some plans that essentially pay you for signing up. This is called “Part B giveback” and is when you get a rebate off of your Medicare premium. On the high end, Medicare Advantage Plans can reach upwards of around $100 per month in Texas. I have found, however, that many of the most popular plans stay between $0 and $47 per month. It is important to note that in contrast to Medicare Supplements, Medicare Advantage Plan premiums are the same for everyone enrolled in the plan. The premiums do not differ based on age, health, or claims.

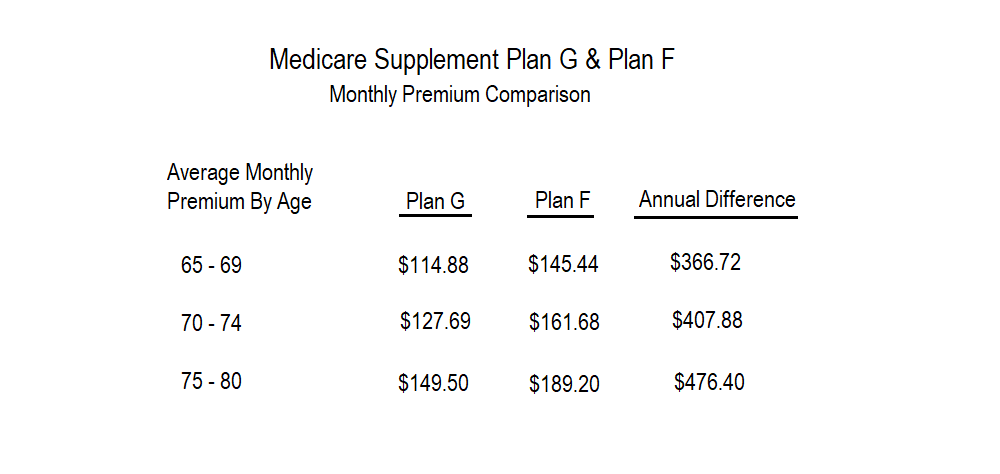

As I said, Medicare Supplements are a little pricier than Medicare Advantage. Monthly premiums for Medicare Supplements in Texas range from $40 a month on the low end to upwards of $250 a month on the high end. Unlike Medicare Advantage, how much you pay can depend on several factors; Your age, zip code, sex, and tobacco status. For the most popular Medicare Supplement Plans, you can realistically expect to pay between $75 and $150 per month, depending on all of your factors.

Winner: Medicare Advantage

Area 2 – Coverage

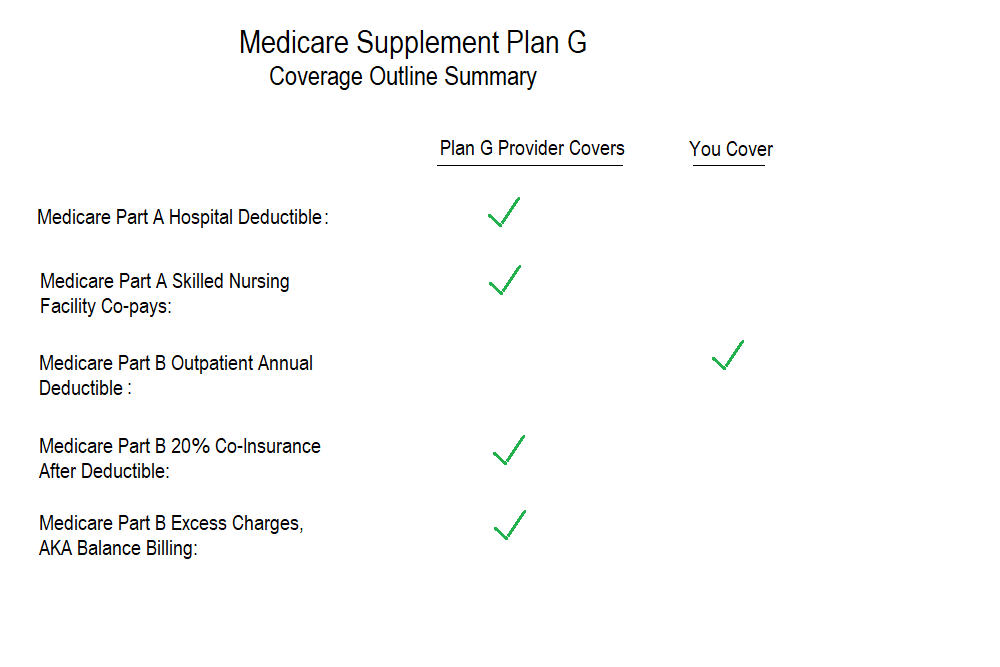

With insurance, coverage is typically defined by how much protection a policy provides. Therefore, how much the insurance pays for and how much liability is left for you. When comparing Medicare Supplements vs. Medicare Advantage, Medicare Supplements will provide you with more coverage. For two of the Most Popular Medicare Supplements, G and F (related article: Plan G – The Best Medicare Supplement), your out of pocket costs for Medicare covered services is between $0 and $185 per calendar year in 2019. This is, as you can see, very rich coverage and low out of pocket costs for you.

Medicare Advantage Plans do help limit your costs, but not as low as Medicare Supplements. With Medicare Advantage Plans, you may have deductibles, co-pays, or co-insurance when you receive medical care. Anytime you pay out of pocket for your medical care, it goes toward your annual out of pocket maximum. Once this out of pocket maximum is reached, your plan will cover 100% of medical costs for the remainder of the year. On average, the annual out of pocket maximums for Medicare Advantage Plans is between $3,400 and $6,700 per year. As you can see, this is significantly higher than Medicare Supplements.

Winner: Medicare Supplements

Area 3 – Doctor Networks

The third area of consideration is doctor & medical provider networks. Medicare Supplements do not manage networks whereas Medicare Advantage Plans do. As mentioned earlier, Medicare Supplements are secondary insurance to Medicare A & B. Medicare Supplements help pay for any medical service covered by Medicare, at any doctor who provides it. Having Medicare and a supplement gives you the flexibility to see any doctor in the country, as long as they accept Medicare for insurance.

Part of what make Medicare Advantage Plans work is containing medical costs. They do this partially by creating agreements with doctors, hospitals, & other medical providers. By having an agreement with a particular Medicare Advantage Plan a doctor is considered “in network” and has agreed to accept members covered under that plan. The two main types of plans are HMO’s and PPO’s. Each of these plan types varies in how strict they are with accessing doctors. HMO’s are the more strict of the two and will only cover you at network doctors, except in cases of emergency. PPO’s will cover you at in network doctors, but also give you the ability to go to out of network at higher costs.

Winner: Medicare Supplements

Area 4 – Part D Prescription

Most Medicare Advantage Plans include Part D prescription coverage built into the plan. Part D is insurance for medications that you fill at the pharmacy. These can be medications that you fill regularly or from time to time. The monthly premium cost that you pay for your Medicare Advantage Plan includes the Part D and in most cases there is no extra premium. Having Part D included with your Medicare Advantage is beneficial because you don’t have to look for and pay extra for prescription coverage.

Medicare Supplement’s primary function is to help you pay for medical costs. As mentioned earlier, Medicare Supplement’s are secondary to Medicare A & B, which covers medical care. When you have a Medicare Supplement, you will need a separate Part D Plan to cover prescriptions you fill at the pharmacy. The negative to this is that you have to get a separate policy and pay an additional premium. The good news is that, in my experience, the most popular Part D plans range from about $20 – $30 per month. There is a positive to having to get a separate Part D Plan; Choice. With Medicare Advantage Plans you must use the prescription coverage that is included with the plan, which could be good or bad. With Medicare Supplements, you can select a Part D prescription plan from the array of choices that best suits your needs.

Winner: Tie

Area 5 – Extra Benefits

To add more value for members, Medicare advantage insurers have began to include dental, vision, and other extra benefits with their plans. These extra benefits are often included with the plan for no cost or as an optional package for an additional premium. Extra benefits can include coverage for teeth cleanings, fillings, and other dental care. On the vision end, $0 cost annual eye exams and an eye wear allowance are typical. A popular benefit often included with Medicare Advantage Plans is Silver Sneakers. With this program you get access to a network of participating gyms & health clubs for no cost. Some Medicare Advantage Plans are even including hearing benefits, which can help cover the cost of exams & hearing aids. The availability and generosity of these benefits with Medicare Advantage will vary based on the particular plan and where you live.

Extra benefits included with Medicare supplements are not as generous as with Medicare Advantage. As mentioned earlier, having a Medicare supplement is going “a la carte” vs getting a “value meal” with Medicare advantage. So, if you want coverage for dental, vision, etc.; you’ll have to buy a separate policy. Many insurance providers are now making individual dental, vision, and hearing plans available for purchase. Medicare Supplements can, however, include some extra benefits with your policy. This is usually in the form of discounts for services in these extra areas previously mentioned. As with Medicare Advantage, extra benefits included Medicare Supplements will vary with each company providing the insurance.

Winner: Medicare Advantage

One More Important Thing To Consider

In addition to comparing the features of Medicare Supplements & Medicare Advantage, it is good to look at the future implications of your either choice. What I mean by this is how difficult it will be to switch to one or the other if you change your mind. With Medicare Supplements, there are less opportunities for open enrollment than with Medicare Advantage. Open enrollment periods are time frames where you can sign up for a plan without answering health questions and having to qualify based on your health.

For Medicare Supplements, you have an open enrollment 6 months before and 5 months after the month you turn 65 or start Medicare Part B. Times where you may start Part B outside of turning 65 are if you deferred enrollment because you were working or if you are under 65 and on disability. Outside of the 6 month open enrollment period, there are times when you have a “guaranteed right” to enroll in a Medicare Supplement Plan. One example is the “trial right,” which gives you the ability to change to a Medicare Supplement if you do so within a year of enrolling in a Medicare Advantage Plan. Outside of qualified open enrollment or guaranteed periods, you are able to apply for a Medicare Supplement anytime throughout the year. You will just need to qualify and answer health questions on your application. If you have to have your health reviewed, do not let this discourage you from applying. There are many options available and the health qualification standards may not be as strict as you think. For details on eligibility for Medicare Supplement insurance, read pages 21 – 23 of the Guide To Health Insurance For People With Medicare.

Medicare Advantage Plans give you many opportunities to enroll and you will never have to qualify based on your health. Similar to Medicare Supplements, you can enroll in a Medicare Advantage Plan 3 months before and after the month you turn 65 or start Part B. This is called your Initial Enrollment Period. Also, from October 15th through December 7th each year, you can change your Medicare Advantage Plan or sign up for the first time. This is called the “Annual Enrollment Period.” There are other periods where you can enroll in a Medicare Advantage Plan known as “Special Enrollment Periods,” which are special situations. For details, click here to visit Medicare.gov Special Circumstances page.

Conclusion

Choosing either a Medicare Supplement or Medicare Advantage for your coverage is often an important decision that has to be made. Going in either direction will affect how much you pay for your insurance premiums. Just as important; It will affect how and where you receive care as well as how much you pay out of pocket when you receive it. In reviewing the chart and comparison above, the question is; which type of plan is right for you? The answer to this depends much on your personal needs, preferences, and your budget for insurance. Another important consideration is how easy it will be for you to change to one or the other in the future. As an objective Insurance Agent, I am not biased to either of these plan types. In my experience both can be good, depending on which is most suitable for your particular situation. With either Medicare Supplement or Medicare Advantage, there are usually lots of good options. Being covered by either is, in my opinion, better than just having Medicare A & B.

We are always happy to provide you with personalized information your eligibility and available plans. Click here to navigate to our request information page.

Thanks for reading!

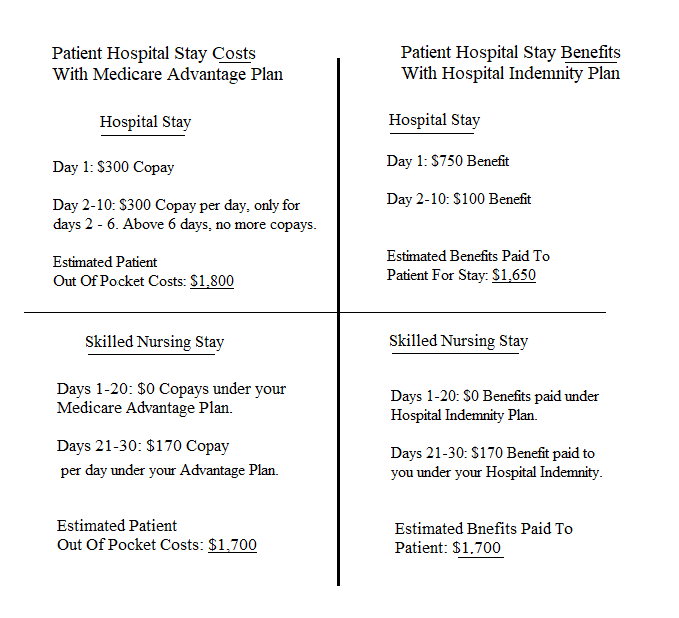

As you can see, having a Hospital Indemnity plan can really help in this situation. Although this is just an example, I have seen real life situations very similar to this one. Needless to say my clients were grateful that they had the Hospital Indemnity coverage. By paying you a cash benefit if you are hospitalized; Indemnity insurance can help protect your savings and from having to pay large out of pocket costs.

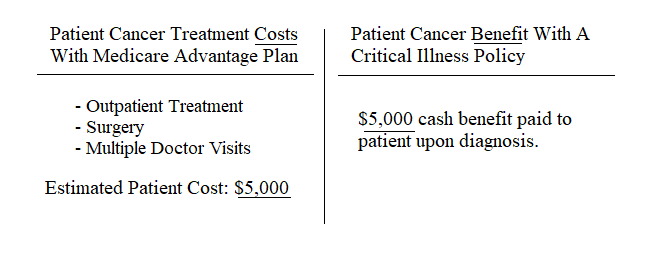

As you can see, having a Hospital Indemnity plan can really help in this situation. Although this is just an example, I have seen real life situations very similar to this one. Needless to say my clients were grateful that they had the Hospital Indemnity coverage. By paying you a cash benefit if you are hospitalized; Indemnity insurance can help protect your savings and from having to pay large out of pocket costs. As you can see in this situation, a Critical Illness policy can help you cover large out of pocket expenses that could reach into the thousands of dollars. It’s very likely that the treatment costs for this situation would end up reaching the individual’s out of pocket maximum for the year. The reality is, we just never know if or when this can happen to us. Having Critical Illness coverage can really be a relief and could quite literally be a life saver.

As you can see in this situation, a Critical Illness policy can help you cover large out of pocket expenses that could reach into the thousands of dollars. It’s very likely that the treatment costs for this situation would end up reaching the individual’s out of pocket maximum for the year. The reality is, we just never know if or when this can happen to us. Having Critical Illness coverage can really be a relief and could quite literally be a life saver.